Country Brief: Sustainable Cooling for All in Kenya

The need for sustainable cooling for all in Kenya

Cooling and cold chains are vital for healthcare and vaccines, for nutrition and agricultural value chains, for thermal comfort at home, work, school, in transportation, and for industrial processes and data centres. Affordable and sustainable cooling is essential for a thriving society and a healthy nation, sitting at the intersection of the Paris Climate Agreement, the Kigali Amendment of the Montreal Protocol and the UN Sustainable Development Goals.

However, millions in Kenya lack access to affordable, reliable, sustainable cooling solutions, exposing them to severe health, wellbeing, and socioeconomic consequences. Regions like the Rift Valley, Northeastern, Eastern, and Coast face the most extreme temperatures. In these hottest regions, according to Chilling Prospects analysis, there are 9.6 million rural and urban poor at high risk due to a lack of access to cooling because they live below the international poverty line (less than USD 2.15 per day, set by the World Bank) in substandard housing and do not have access to electricity. There are a further 14.8 million lower-middle-income people at medium risk due to a lack of access to cooling who also live without access to electricity and, although not impoverished, have limited financial resources to purchase cooling services.

For Kenyans with access to electricity, refrigeration and air-conditioning (RAC) usage is increasing due to rising incomes, temperatures, and heatwaves and will impact Kenya’s energy systems and climate goals. Based on analysis from GIZ in the report Greenhouse Gas Inventory for the Refrigeration & Air Conditioning Sector in Kenya, the 2022 National Cooling Action Plan for Kenya (NCAP) projects that the combined direct and indirect emissions from RAC, currently at approximately 4 Mt CO2eq in 2030, could reach 7.87 Mt CO2eq in 2050 under a ‘business as usual’ scenario, through a combination of refrigerant leakage, appliance end of life, and energy use. To align with national energy and climate strategies, these emissions need to be abated.

With the recent release of Kenya’s Energy Transition and Investment Plan 2023-2050 (ETIP), which outlines Kenya’s path to achieving Net Zero by 2050 while growing the economy and leveraging green growth opportunities, and the government's commitment to the Global Cooling Pledge, it is a timely moment to reassess cooling requirements to meet Kenya’s societal, health and economic goals whilst underscoring the important role of cooling in supporting Kenya's energy transition and climate goals and ensuring no one is left behind.

This country brief presents Kenya’s cooling needs, discusses challenges and opportunities, including those related to its significant agriculture sector, reviews the solutions necessary to advance sustainable cooling for all in Kenya, and recommends priority areas for policy and market interventions that would advance sustainable and equitable cooling for all in Kenya. Details can be explored in the full report.

Climate

The climate [1] in Kenya varies. The coast is typically hot and humid whilst the country’s northern and northeastern areas are generally very hot and arid. Inland areas are more temperate, and the central highlands are cooler.

Historic average temperatures for Kenya range from a nighttime minimum of 18.3°C to daytime maximum of 30.3°C. However, the Rift Valley, Northeastern, Eastern and Coast provinces experience much higher heat exposure, especially during the dry seasons. Turkana County in the north of the Rift Valley Province is significantly hotter than the rest of the county, with monthly average highs close to 40°C.

Kenya’s temperatures could rise by as much as 3.5 Celsius degrees [2] by the end of century under a ‘business as usual’ climate scenario (i.e. Representative Concentration Pathway 8.5 by a World Bank 2021 study)1. Even under the “middle of the road” scenario (Shared Socioeconomic Pathway, or SSP, 2-4.5) rising temperatures will be significant and there will be more hot days experienced – see figure below.

Figure 2: Projected number of annual hot days where the maximum temperature exceeds 35°C across Kenya under climate scenario SSP2-4.5; 50th percentile.

Population and Economy

Kenya has a diverse and youthful population [3] of over 55 million people, with a significant portion (29.5 percent) residing in urban areas like Nairobi and Mombasa. 36 percent of the total population live below the poverty line and 51 percent of the urban population live in informal, or slum, housing.

The economy is the largest in East Africa, driven by agriculture (approximately 33 percent of GDP), tourism, manufacturing, and services, with recent growth in technology and innovation sectors positioning Kenya as a regional economic hub.

More than half of the population live in the hottest provinces of Kenya - the Rift Valley, Northeastern, Eastern and Coast.

Electricity Access, Power Generation and Carbon Emissions

Kenya's power generation is predominantly from renewable energy sources, currently over 90 percent, with significant contributions from geothermal and hydro. Access to electricity has improved considerably, with 98 percent of urban populations having access. However, rural areas still face challenges in achieving full electrification (65 percent), making the country’s access total 76.6 percent in 2022. [4]

The country’s Energy Transition and Investment Plan provides a pathway to net zero by 2050 that includes a significant increase in the capacity of renewable power generation to plug electricity access gaps and meet the country’s growing electricity demand that is driven substantially by income growth.

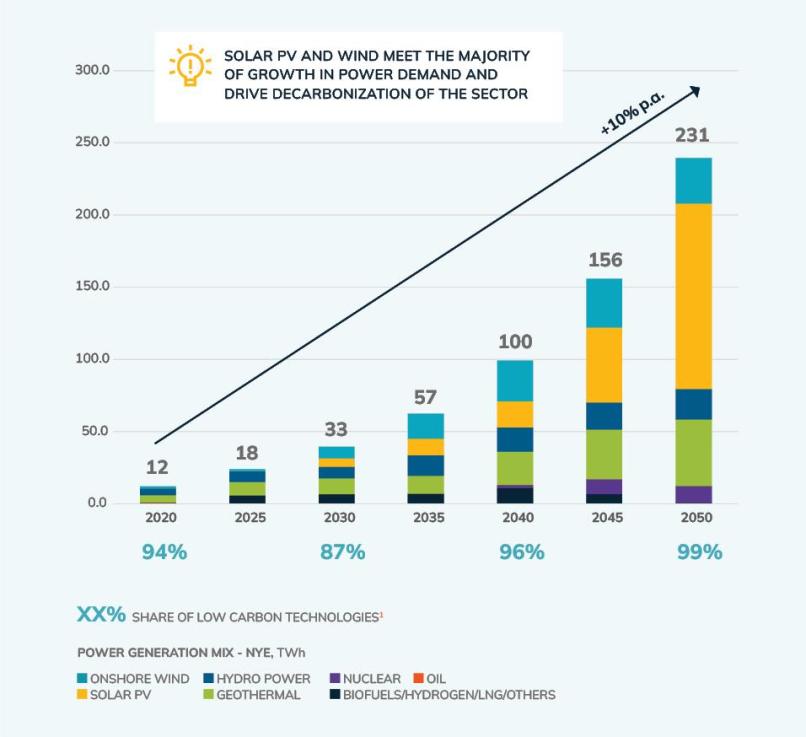

In 2020, power generation was 12.02 TWh, predominantly generated by geothermal (42 percent) and hydro power (39 percent). The associated electricity grid carbon factor was 56.81 gCO2/kWh and total annual carbon emissions from power generation 0.68 MtCO2.

By 2050 Kenya’s annual power generation necessary to meet electricity demand is projected to be 239.40 TWh, 20 times more than that in 2020, with an electricity grid carbon factor of –0.07 gCO2/kWh (negative due to a portion of power being generated through biomass with carbon capture and storage).

New solar PV, wind and geothermal meet most of the power generation increase in 2050. Some growth is met with nuclear and hydro, as far as available resources allow. Under the plan, unabated fossil fuels are phased out by 2040, with storage playing the key balancing role. Around two thirds of the power demand is driven by powering industry and buildings, with the remaining third driven by demand from transport and hydrogen production. Cooling systems are needed across all these sectors, and it is necessary to limit cooling demand such that it does not undermine the net-zero pathway.

Cooling Access

Within the hottest regions of Kenya – the Coast, Eastern, Northeastern, and Rift Valley provinces – Chilling Prospects analysis shows that:

9.6 million people are at high risk due to a lack of access to cooling. This includes 5.1 million rural poor who lack electricity and live in extreme poverty, often engaging in subsistence farming without access to intact cold chains, and 4.5 million urban poor with limited or no electricity access, living in thermally poor housing and facing intermittent electricity supplies.

Outside the analysed hot regions, cooling access remains a challenge, exposing many to the harmful effects of heat without adequate adaptation. For example, small-scale fishermen in Homa Bay lack cold chain infrastructure, and residents of Nairobi's informal settlements like Kibera, Mathare, and Mukuru live in poorly constructed homes that intensify heat. As a result, temperatures in these areas often exceed those in formal Nairobi neighbourhoods, reaching levels that pose health risks, particularly for children and the elderly.

Notes and references:

[1] Climate Risk Profile: Kenya (2021): The World Bank Group

[2] World Bank (n.d), Climate Change Knowledge Portal, Retrieved 16 August 2024

[3] World Bank Group (2023), World Development Indicators; Food and Agriculture Organization of the United Nations (n.d). Kenya at a glance, Retrieved August 16 2024; and 2019 Kenya Population and Housing Census: Volume 2 Distribution of Population by Administrative Units.

[4] IEA, IRENA, UNSD, World Bank, WHO. 2023. Tracking SDG 7: The Energy Progress Report. World Bank, Washington DC.

Related content